XMU professor’s work ranks among top-cited JFM articles

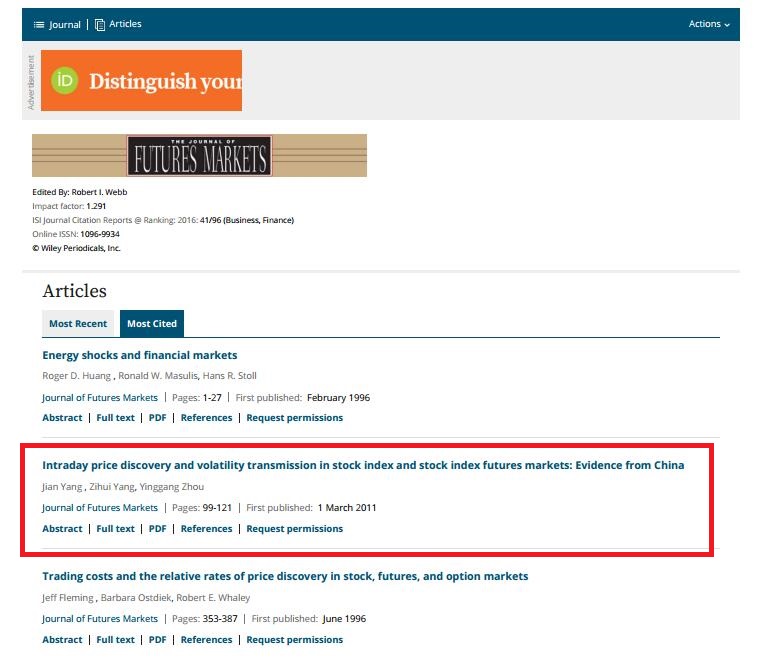

According to the news released by the Journal of Futures Markets (JFM) recently, the article “Intraday Price Discovery and Volatility Transmission in Stock Index and Stock Index Futures Markets: Evidence from China”, which is co-authored by Professor Yinggang Zhou from XMU, Professor Jian Yang from the University of Colorado (Denver Campus) and Professor Zihui Yang from Sun Yat-Sen University, has been selected as one of the most cited articles published by JFM. JFM is known as a prestigious international journal covering latest developments in financial futures and derivatives. According to the statistics by Google Scholar, this article has been cited 156 times by scholars from home and abroad since its official publication in 2012.

The article was officially published in the Journal of Futures Markets, Vol. 32, No. 2, in 2012, hailed as the first paper on China’s stock index futures in the world’s top financial journals. By virtue of a novel empirical econometric model and high-frequency data, this study investigates intraday price discovery and volatility transmission between the Chinese stock index and the newly established stock index futures markets in China. And the research found that the launch of China’s stock index futures is not the actual cause for the steep decline of the Chinese stock index.

China Stock index futures can be regarded as China's first successfully-launched financial product of futures. Within three years, it was ranked among the world's top ten futures contracts of the highest trading volume. This article has spearheaded the studies on the financial innovation of China, namely China stock index futures, at the international level. Meanwhile, it also serves as a reference for the researches on the emerging futures markets of varied types in China.

Yinggang Zhou, Ph.D. in Finance from XMU and Ph.D. in Economics from Cornell University, is currently a dually-employed professor of XMU. His main research areas include asset pricing, financial risk management, international finance and trade, etc. He has published more than 30 papers in various prestigious journals such as Management Science, Journal of Banking and Finance, Journal of Futures Markets and Real Estate Economics.

Source: http://news.xmu.edu.cn/19/4d/c1552a334157/page.htm

Edited by Wu Qianyi